Latest Relaxation For GST & Income Tax due to Covid-19

In view of the adverse circumstances arising due to the severe Covid-19 pandemic and also in view of the several requests received from taxpayers, tax consultants & other stakeholders from across the country, requesting that various compliance dates may be relaxed regarding GST & INCOME TAX, the Government has extended certain timelines.

GST Relaxation:

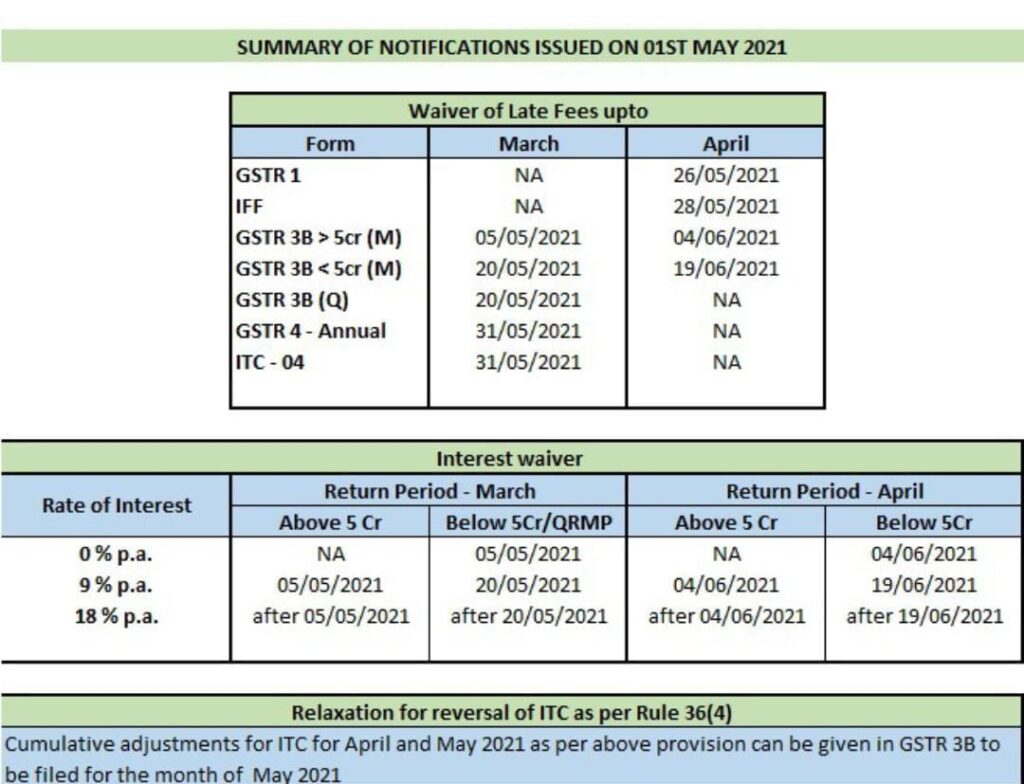

As per a set of notifications issued by the CBDT and CBIC), the Government has waived off the late fee for GSTR-3B for the months of April and May 2021. The exemption is available for a delay of up to 15 days and 30 days from the original due date for taxpayers with a turnover of more than 5 crores and up to 5 crores respectively for the quarter ending 31st Mar, no late fees if 3b filed by 30 days from the original due date.

GSTR-4 due date extended to 31st May Further, the deadline for ITC-04 has been extended to 31st May for the Jan-Mar quarter. (Notification no. 10/2021, – 11/2021 CGST)

GSTR-1 due date for April’21 extended to 26th May and IFF due date extended to 28th May. (Notifications no. 12/2021 – CGST)

Restriction of 10% Provisional ITC shall be applicable for cumulative for April 2021 & May 21 in form GSTR 3B for May 21. (Notification no. 13/2021 – CGST)

any time limit for completion of any action, by any authority or by any person, specified in, or prescribed or notified under rule 9 of the Central Goods and Services Tax Rules, 2017, falls during the period from the 1st day of May 2021 to the 31st day of May 2021, and where completion of such action has not been made within such time, then, the time limit for completion of such action, shall be extended up to the 15th day of June 2021;

Timeline for all other proceedings, asset order, etc. Whose the last date of completion falls between 15th April to 30th May is extended to 31st May.

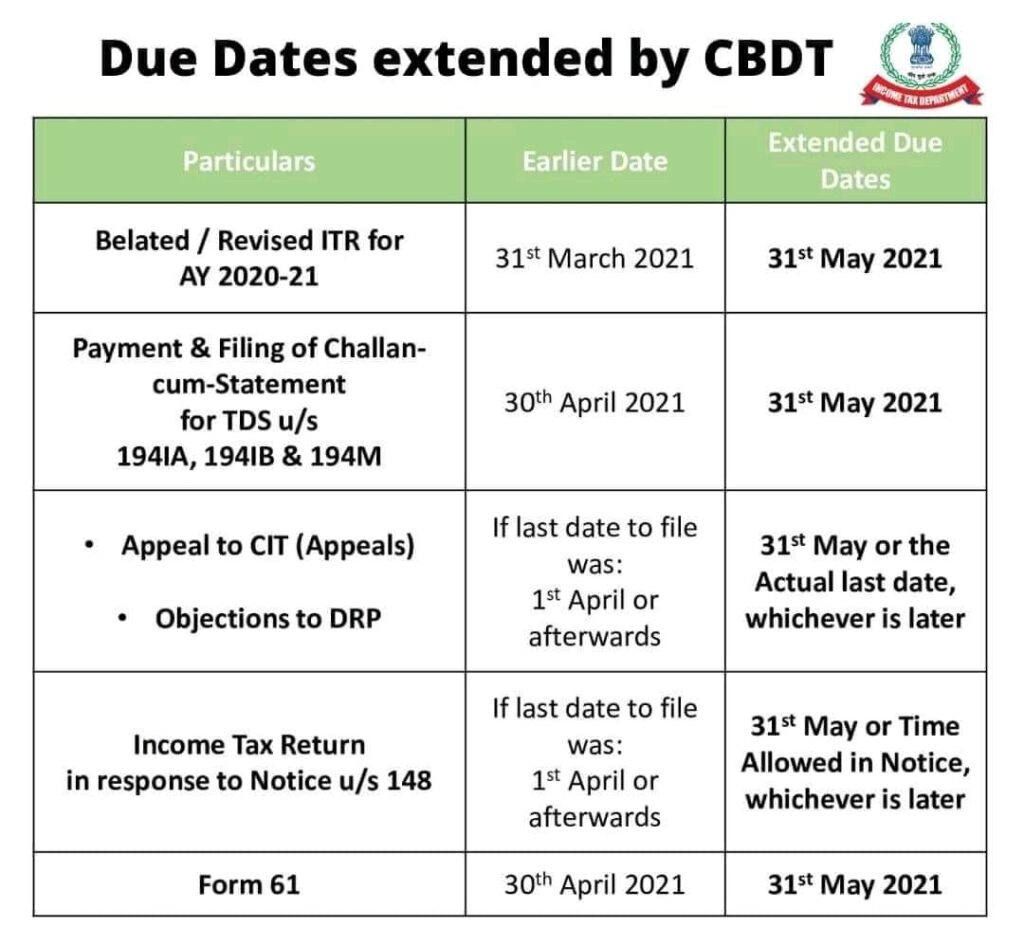

Income Tax Relaxation :

➢ Filing of belated / Revised Income Tax Return For FY 2019-20 ( AY 2020-21) under sub-section (4) and revised return under sub-section (5) of Section 139 of the Income-tax Act,1961 for Assessment Year 2020-21, which was required to be filed on or before 31 ” March 2021, may be filed on or before 31″ May 2021 ;

➢Appeal to Commissioner (Appeals) under Chapter XX of the Income-tax Act, 1961 for which the last date of filing under that Section is 1″ April 2021 or thereafter, may be filed within the time provided under that Section or by 31″ May 2021, whichever is later;

➢ Objections to Dispute Resolution Panel (DRP) under Section 144C of the Income-tax Act, 1961, for which the last date of filing under that Section is 1″ April 2021 or thereafter, may be filed within the time provided under that Section or by 31″ May 2021, whichever is later;

➢ Income-tax return in response to notice under Section 148 of the Income-tax Act, 1961, for which the last date of filing of return of income under the said notice is 1″ April 2021 or thereafter, may be filed within the time allowed under that notice or by 31″ May 2021, whichever is later;

➢ Payment of tax deducted under Section 194-IA, Section 194-IB, and Section 194M of the Income-tax Act, 1961 and filing of challan-cum-statement for such tax deducted, which are required to be paid and furnished by 30’h April 2021 under Rule 30 of the Income-tax Rules, 1962, maybe paid and furnished on or before 31″ May 2021.

➢ Statement in Form No. 61, containing particulars of declarations received in Form No.60, which is due to be furnished on or before 30’h April 2021, maybe furnished on or before 31″ May 2021

.